Where You Go Matters (And Not Just Medically)

How ER, Urgent Care, and Primary Care (PCP) Work Behind the Scenes — and Why It Affects Your Coverage

It’s 9:12 PM.

Something doesn’t feel right.

Maybe it’s chest pain.

Maybe it’s a fever that won’t break.

Maybe it’s a sharp pain that started an hour ago and won’t go away.

You start running the mental checklist.

Is this ER-level?

Is this urgent care?

Can this wait until morning to call my primary care doctor?

You open Google.

You close Google.

You text someone who may not be a medical professional but definitely has strong opinions.

Most of the advice you’ll find focuses (appropriately) on the medical decision — and that’s important. Safety always comes first.

But today, I want to talk about something different.

I want to talk about what happens operationally and administratively once you choose.

That choice determines:

how your visit is billed,

how your claim is processed,

how your deductible shows up,

and whether you later say, “Wait… why are there three bills?”

This blog is not medical advice.

It’s the “what happens after the visit” version.

And no, this is not about turning you into a healthcare accountant at 9:12 PM.

It’s about understanding the system before 9:12 PM ever happens.

Medical Guidance vs. Systems Guidance (Guardrails Included)

Before we go any further, I want to say something clearly.

If something feels life-threatening, unstable, or truly emergent — go to the Emergency Room. Full stop.

Cost should never be the reason someone avoids life-saving care.

This post is not about discouraging ER visits.

It’s not about blaming people for “overusing” the system.

It’s not about telling you to do deductible math when you’re in pain.

Medical safety always comes first.

If you’re looking for thoughtful, practical guidance on when to choose the ER versus urgent care or primary care (PCP) from a clinical perspective, I highly recommend following Dr. Brian Kendall. His Substack includes posts like his “ER 101 series” and “ER, Urgent Care, or Primary Care” that walk readers through medical decision-making in a clear, grounded way. (https://substack.com/@briankendallmd)

This piece complements that perspective.

We’re going to focus on what happens after you walk through the door, how claims are processed against your benefits, how site of service changes your financial experience, and why understanding your coverage ahead of time can reduce stress later.

You deserve to make the safest decision in the moment, without being blindsided later.

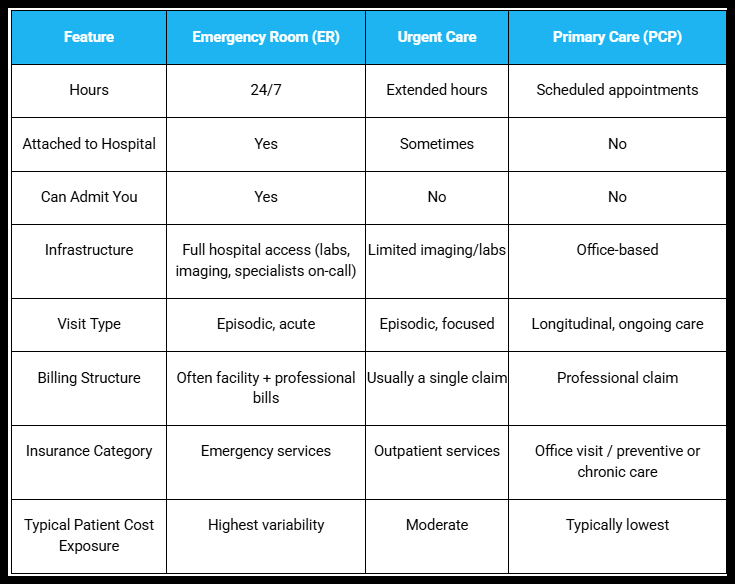

The Three Doors - And What Changes Behind Them

At a high level, the Emergency Room, Urgent Care, and your Primary Care Physician all provide medical care.

But operationally?

They are built very differently.

Different staffing models.

Different capabilities.

Different billing structures.

Different insurance categories.

And those differences matter. Not because one is “good” and one is “bad”, but because they trigger different administrative pathways once a claim is submitted.

Here’s a simple side-by-side view:

Urgent Care, ER, Primary Care Comparison

Now let’s simplify this a little.

Each of these settings is built for something different.

When you walk into an ER, you’re walking into a hospital environment that is prepared for the most serious situations at any hour of the day. Trauma teams. Immediate imaging. Specialists on call. The ability to admit you upstairs if needed.

It’s designed for “what if this is the worst-case scenario?”

Urgent care is built for things that need attention today, but aren’t life-threatening. Think stitches, sprains, infections, high fevers, things that can’t wait a week but don’t require a hospital-level response.

Primary care is different. Your PCP isn’t just treating one moment; they’re managing your overall health over time. They know your history. Your patterns. Your medications. What’s normal for you and what isn’t.

That familiarity matters.

They’ve seen you when you’re well. So when something changes, they can better judge whether it’s serious or manageable.

The ER is built for life-or-death possibilities.

Urgent care is built for “this can’t wait, but it’s not critical.”

Primary care is built for prevention and pattern recognition.

Those structural differences are what drive the administrative differences that follow. And here’s where insurance enters the picture. Your insurance plan doesn’t treat all visits the same — even when the symptoms might look similar at first.

Let’s say you have abdominal pain.

If it’s severe, sudden, and concerning for something life-threatening, the ER is absolutely the right choice. But sometimes abdominal pain could reasonably start in the urgent care setting. Or with your primary care physician. Or escalate from one to another.

And that’s where the administrative differences begin.

Insurance plans sort care into categories:

Emergency services

Hospital Outpatient Service (Urgent Care)

Office visits

Preventive care

Each of those categories has its own cost-sharing rules inside your plan.

So:

If you walk into the ER, the claim is processed under your emergency benefit.

If you walk into urgent care, it’s often processed under outpatient services.

If you see your PCP, it’s processed as an office visit.

Not because your body changed. But because the place where you received your care changed.

And that site determines which part of your benefits gets activated.

What Those Categories Mean for Your Wallet

Now let’s talk about what those benefit categories actually mean in real life.

When you use your insurance, there are two parts to how it works:

What you pay every month (your premium).

What you pay when you actually receive care.

That second part is called cost-sharing.

Cost-sharing means the portion of the medical bill you are responsible for.

That can show up in a few ways.

We’re not going deep into all the details here — it truly deserves its own blog (and it’s available if you’d like to read it).

Here is the simple version.

A deductible is the amount you pay out of pocket before your insurance starts sharing costs.

Think of it as the first layer. Until that amount is met for the year, you’re covering most of the bill.

For example, if you have a $2,000 deductible, that amount must be met first.

A copay is a flat fee for certain types of visits.

For example:

$25 for a primary care visit.

$75 for urgent care.

It’s predictable. It doesn’t change based on how much the visit costs.

Coinsurance is a percentage you pay after your deductible is met.

For example:

Insurance pays 80%.

You pay 20%.

That’s it. That’s the simple version.

Now here’s where the door you choose matters.

Emergency Room visits often involve higher cost-sharing. Some plans require a large ER copay. Others apply the visit directly to your deductible first. Many include coinsurance after that.

Urgent care visits are often lower-cost than the ER and may have a smaller copay, though some plans still apply them to the deductible.

Primary care visits typically have the lowest copays. Preventive visits are often covered at 100%, as long as they stay within preventive guidelines.

The exact numbers depend on your specific plan.

But the pattern is consistent:

The more intensive the setting, the more likely it is to trigger higher cost-sharing.

What I’m describing here are common patterns.

But insurance plans are built differently. The only way to know exactly how your plan applies deductibles, copays, and coinsurance is to look at your Summary of Benefits. You can usually get this from your HR department or find it in your insurance member portal.

Look specifically at how your plan lists:

Emergency Room care

Urgent care

Primary care visits

Don’t Wait Until 9:12 PM to Learn Your Benefits

Emergencies can’t be scheduled.

They don’t check your deductible first.

They don’t wait for open enrollment.

They don’t care whether you’ve met your out-of-pocket maximum.

And when you’re in the middle of something scary or painful, that is not the moment to be wondering:

“Wait… how is this covered?”

This isn’t about discouraging care.

It’s about removing one layer of uncertainty before you ever need to use it.

If you’re in pain, if something feels wrong, if it feels urgent — you go.

You get treated.

You breathe again.

The symptoms ease.

The crisis passes.

And then, a few weeks later, an envelope arrives.

Or three.

And that’s when the second wave hits.

Not physical pain.

Financial confusion.

“Why are there multiple bills?”

“Why did this go to my deductible?”

“I thought this was covered.”

“Did I go to the wrong place?”

That feeling, the surprise, the scrambling, the not knowing, shouldn’t feel more painful than the actual visit.

Understanding how your benefits work ahead of time isn’t about choosing cost over safety.

It’s about reducing that second wave.

Because after the medical moment passes, life keeps moving. Recovery begins. Follow-up appointments happen. Questions come up.

And this is where having the right kind of care and the right kind of relationship starts to matter differently.

Here’s What I’ve Learned About Primary Care

This is my opinion.

It’s shaped by my own health journey, by navigating specialists, urgent visits, prescriptions, follow-ups, and more paperwork than I ever expected to understand.

And one thing has become very clear to me:

Having a primary care physician has changed how I experience healthcare.

Not because emergencies disappear.

But because I am not starting from zero every time something happens.

My PCP knows my baseline.

They know what’s normal for me.

They know my history.

They know which symptoms are new — and which ones are part of a longer pattern.

And when you live with something ongoing, that difference is everything.

Primary care is often preventive, things like annual checkups, screenings, and routine monitoring.

The good news is that these preventive visits are usually covered by insurance without you having to pay anything out of pocket, as long as the appointment stays focused on prevention rather than diagnosing a new problem.

That makes it easier to stay connected before something turns into a late-night decision.

But the real value, for me, has shown up in the in-between.

When I’m unsure where to go, I can call.

I can send a message.

I can ask, “Is this something we monitor?”

“Does this need urgent care?”

“Is this ER-level issue?”

Sometimes the answer has been, “Let’s watch it.”

Other times, it’s been, “Go now.”

There was one moment where something was clearly off. My PCP recognized it immediately. They didn’t just tell me to go to the ER; they called ahead. They gave the ER a summary of what was happening and why I was coming.

I’m not saying every primary care physician will do that.

But in that moment, I wasn’t just a chart.

I was a person with context.

And that changed everything.

Primary care also helps with the parts people don’t see.

Coordinating specialists.

Managing prescriptions.

Following up on test results.

Making sure referrals actually go through.

It reduces the feeling of being bounced from one door to another.

It creates continuity in a system that often feels fragmented.

There are different ways to structure that relationship, too. Some people access primary care through traditional insurance networks. Others choose Direct Primary Care (DPC), where you pay a monthly fee directly to a physician for more access and fewer insurance barriers.

I’m not recommending one model over another.

But the underlying value is the same:

Having someone who knows you.

Not just your symptoms, you.

It doesn’t eliminate emergencies.

It doesn’t replace urgent care.

But it changes how you enter those moments.

And for me, that has made the system feel less chaotic.

More human.

Wrapping Up

Where you go matters.

Medically, always.

Operationally and financially, too.

If something feels life-threatening, unstable, or truly urgent, GO. Safety comes first—every time.

Outside of those moments, take a few minutes to understand how your plan works.

Look at your Summary of Benefits. Know how your plan handles Emergency Room visits, urgent care, and primary care. Understand what deductible, copay, and coinsurance mean for you.

Not so you can override a medical decision.

But so you’re not surprised later.

The ER, urgent care, and primary care all serve important roles. They exist for different reasons. They’re built differently. And because they’re built differently, your insurance responds differently.

Understanding that won’t eliminate complexity.

But it can reduce confusion.

And when you’re already navigating something hard, that clarity matters.

Thanks for reading,

Bonnie

Next Up

Now that we’ve talked about where you go, ER, urgent care, or primary care, the next question becomes:

What actually happens after the visit?

In the next post, we’ll walk through how medical coding works, how claims are processed, and why what’s documented in your chart can directly affect how your benefits apply.

Because once you understand the doors, it helps to understand the language behind them.

👋 Disclaimer: This blog is for educational purposes only and reflects my perspective and experience. It’s not legal, financial, or medical advice. Always check with your insurance company, healthcare provider, or HR department for guidance on your specific plan and coverage.

My goal is to help you better understand how the system works so you can be a more confident advocate for yourself and your loved ones.

Subscribe or learn more at www.coviewconsulting.com